2026 VA Loan Limits and County Reference Guide for Veterans Home Loan Financing

The VA Nationwide Home Loan Team Offers Non-Conforming Solutions Up to $3 Million +. Helping Service Members and Veterans Maximize Their Home Loan Benefits

Written by the VA Nationwide Lending Team, powered by The Federal Savings Bank, NMLS# 411500

Last Updated: November 29, 2025

Our VA loan specialists have helped thousands of veterans, active-duty service members, and military families navigate the home financing process. From straightforward purchases to complex VA construction and renovation projects, we focus exclusively on serving those who have served.

If you've earned VA loan eligibility through your military service, you may be wondering how the 2026 conforming loan limits announced by the Federal Housing Finance Agency (FHFA) affect your options. The short answer: for most veterans, they don't impose a hard cap. But understanding these numbers still matters, especially if you have partial entitlement or want to compare VA financing against conventional alternatives.

Why Veterans Should Understand 2026 County Loan Limits

The FHFA released updated conforming loan limits on November 25, 2025, with the new figures taking effect January 1, 2026. The national baseline for a single-family property increases to $832,750, up from $806,500 in 2025. High-cost areas can reach a ceiling of $1,249,125.

These limits directly govern conventional mortgages backed by Fannie Mae and Freddie Mac. For VA loans, the picture is different. Since the Blue Water Navy Vietnam Veterans Act took effect in January 2020, veterans with full entitlement face no VA-imposed loan limit. You can finance well above $832,750, or any county ceiling, with zero down payment required, provided you qualify based on income, credit, and lender guidelines.

So why does this page exist? Because county conforming limits remain relevant for several groups of VA borrowers, and because veterans often weigh VA financing against conventional or FHA options. Having accurate reference figures helps you make informed decisions.

Full Entitlement vs. Partial Entitlement: What the Numbers Mean for You

Your VA entitlement determines how much of your loan the Department of Veterans Affairs will guaranty. That guarantee allows lenders to offer favorable terms, including zero-down-payment options and no private mortgage insurance.

Veterans with Full Entitlement

If you have never used your VA loan benefit, or if you've fully restored it after paying off a previous VA loan and selling the property, you have full entitlement. For veterans in this category:

There is no maximum VA loan amount. The conforming limits published by FHFA do not restrict you. You can purchase a home for $1 million, $2 million, or more with no down payment, subject to your ability to qualify and the lender's approval.

Your guaranty covers 25% of the loan amount with no cap, giving lenders the assurance they need to offer zero-down financing on higher-priced properties.

County loan limits become reference points rather than restrictions. They may still matter for comparing VA terms against conventional jumbo loans or when evaluating whether a property qualifies for certain pricing tiers.

Veterans with Partial Entitlement

Veterans who currently have an active VA loan, who have defaulted on a previous VA loan, or who sold a home but did not pay off the VA loan in full may have partial entitlement. In these situations, county conforming limits directly affect your financing:

The FHFA county limit determines your maximum guaranty amount. The VA will guarantee 25% of the county limit (minus any entitlement already in use). If your desired loan amount exceeds your remaining entitlement, you may need a down payment for the portion above your available guaranty.

For example, if your county's 2026 limit is $832,750 and you have $100,000 of entitlement tied up in an existing VA loan, your remaining guaranty covers a smaller loan amount. Financing above that threshold typically requires 25% down on the excess.

Understanding your specific entitlement situation is critical before making offers on higher-priced properties. Our team can walk you through the calculation based on your Certificate of Eligibility.

Restoring Your Entitlement

If you've paid off a VA loan and no longer own the property, you can request a one-time restoration of entitlement, making your full benefit available again. In some cases, veterans can also restore entitlement while retaining a previously purchased property, though specific conditions apply. We help veterans navigate these scenarios regularly, and restoration often unlocks zero-down options on your next purchase.

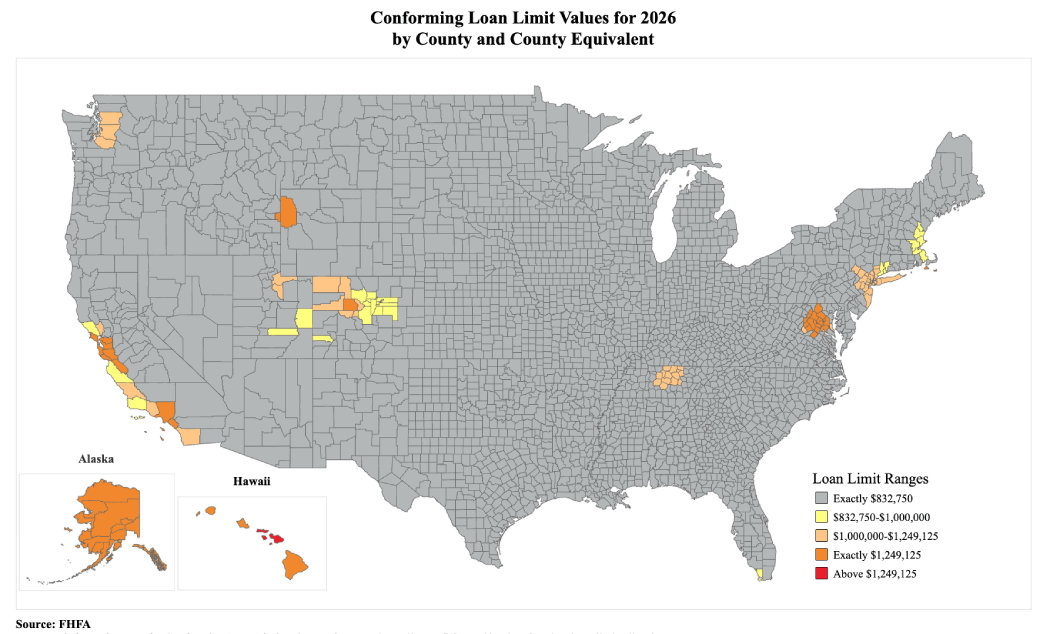

2026 Conforming Loan Limits by County Type

While VA loans aren't capped by these figures for full-entitlement borrowers, the conforming limits serve as baseline references for entitlement calculations, jumbo loan comparisons, and veterans considering conventional alternatives.

Standard County Reference Limits

The majority of U.S. counties (more than 3,000) use these baseline figures:

| Property Units | 2026 Baseline |

|---|---|

| Single-Family (1 Unit) | $832,750 |

| Duplex (2 Units) | $1,066,250 |

| Triplex (3 Units) | $1,288,800 |

| Fourplex (4 Units) | $1,601,750 |

High-Cost County Limits

Roughly 160 counties qualify for elevated limits based on local median home values. The ceiling is set at 150% of the baseline:

| Property Units | 2026 High-Cost Ceiling |

|---|---|

| Single-Family (1 Unit) | $1,249,125 |

| Duplex (2 Units) | $1,599,375 |

| Triplex (3 Units) | $1,933,200 |

| Fourplex (4 Units) | $2,402,625 |

Veterans purchasing in areas like San Diego, the Washington D.C. metro, or parts of the San Francisco Bay Area will see their counties at or near this ceiling. If you have full entitlement, these figures don't limit your VA loan. If you have partial entitlement, the ceiling becomes the reference point for your guaranty calculation.

Alaska, Hawaii, Guam, and the U.S. Virgin Islands

Federal law grants these locations higher baseline limits due to elevated costs of living and construction. For VA borrowers with partial entitlement stationed or purchasing in these areas, the elevated figures provide additional flexibility:

| Property Units | 2026 Baseline | 2026 Ceiling |

|---|---|---|

| Single-Family (1 Unit) | $1,249,125 | $1,873,675 |

| Duplex (2 Units) | $1,599,375 | $2,399,050 |

| Triplex (3 Units) | $1,933,200 | $2,899,800 |

| Fourplex (4 Units) | $2,402,625 | $3,603,925 |

Active-duty members receiving PCS orders to Hawaii or Alaska often have questions about whether their VA benefit stretches far enough. With full entitlement, it does. With partial entitlement, these elevated limits provide more room than mainland figures.

VA Jumbo Loans: Financing Beyond County Limits

Even before the Blue Water Navy Act removed limits for full-entitlement veterans, VA Nationwide specialized in VA jumbo loans for higher-priced properties. Today, these programs remain valuable for veterans who want the benefits of VA financing on homes that exceed conventional conforming thresholds.

VA jumbo loans through our team offer zero down payment with full entitlement, competitive interest rates that often beat conventional jumbo alternatives, no private mortgage insurance regardless of loan size, and flexible credit guidelines compared to traditional jumbo underwriting.

For veterans with partial entitlement, we structure jumbo VA loans that minimize required down payments while maximizing your remaining guaranty. Our VA Jumbo Loans page explains how these programs work and what to expect during underwriting.

How These Limits Compare to Recent Years (2023–2026)

Tracking the progression of conforming limits provides context for market trends and helps veterans understand how their purchasing power has evolved.

| Year | 1-Unit Baseline | 1-Unit High-Cost | Year-Over-Year Change |

|---|---|---|---|

| 2023 | $726,200 | $1,089,300 | — |

| 2024 | $766,550 | $1,149,825 | +5.56% |

| 2025 | $806,500 | $1,209,750 | +5.21% |

| 2026 | $832,750 | $1,249,125 | +3.26% |

The 3.26% increase for 2026 reflects moderating home price growth according to FHFA's third-quarter House Price Index data. For veterans, this slower pace means your VA benefit continues to cover more of the market without requiring limit adjustments to keep up with rapid appreciation.

Multi-Unit Baseline Comparison (2024–2026)

| Year | 1 Unit | 2 Units | 3 Units | 4 Units |

|---|---|---|---|---|

| 2024 | $766,550 | $981,500 | $1,186,350 | $1,474,400 |

| 2025 | $806,500 | $1,033,000 | $1,248,150 | $1,551,250 |

| 2026 | $832,750 | $1,066,250 | $1,288,800 | $1,601,750 |

Veterans interested in purchasing multi-unit properties (up to four units) can occupy one unit and rent the others, using projected rental income to help qualify. This strategy works well for building wealth while leveraging your VA benefit.

Common Questions About VA Loans and 2026 Limits

Do VA loans have limits in 2026?

For veterans with full entitlement, no. The Blue Water Navy Vietnam Veterans Act, effective January 1, 2020, removed VA loan limits for eligible borrowers who have their complete entitlement available. You can purchase above any county limit with zero down payment if you qualify based on income and credit. Veterans with partial entitlement still use county conforming limits to calculate their available guaranty.

What is the difference between full and partial entitlement?

Full entitlement means you have never used your VA loan benefit, or you've restored it after paying off a previous VA loan and selling the associated property. Partial entitlement occurs when some of your guaranty is tied up in an existing VA loan, a previous foreclosure, or a short sale that affected your entitlement. Veterans with partial entitlement may need a down payment on loan amounts that exceed their remaining guaranty coverage.

How do I know my entitlement status?

Your Certificate of Eligibility (COE) shows your current entitlement. You can request a COE through the VA's eBenefits portal, or our team can pull it on your behalf during the loan process. The COE indicates your total entitlement and any amounts currently in use.

Can I have two VA loans at the same time?

Yes, under certain circumstances. If you have remaining entitlement after your first VA loan, you can use it toward a second property. This is common for service members who PCS to a new duty station but keep their previous home as a rental. The second loan amount may be limited by your remaining entitlement, and county limits factor into that calculation.

How do 2026 limits affect VA construction loans?

VA construction loans allow you to finance land purchase and home construction with your VA benefit. For veterans with full entitlement, the 2026 conforming limits don't restrict your construction loan amount. Those with partial entitlement should work with their loan officer to determine how much they can finance based on the remaining guarantee. Our VA Construction Loans page details the one-time close and two-time close options available.

What about VA renovation loans?

VA renovation financing lets you purchase a home and include repair or improvement costs in a single loan. The same entitlement rules apply: full entitlement means no hard limit, while partial entitlement requires calculating your available guaranty against the total loan amount. Renovation loans work well for veterans purchasing homes that need updates, including foreclosures or older properties. Learn more on our VA Renovation Loans page.

Are manufactured homes eligible for VA financing?

Yes. VA loans can finance manufactured homes that meet VA and HUD requirements, including proper foundation certification. The 2026 conforming limits apply the same way as for site-built homes. Our VA Manufactured Home Loans page covers eligibility requirements and financing options for factory-built housing.

What happens if home prices drop? Will limits decrease?

No. Under the Housing and Economic Recovery Act of 2008, conforming loan limits cannot decrease. If home prices decline, limits remain flat until appreciation exceeds previous peaks. This stability protects veterans from sudden changes to entitlement calculations.

Should I choose VA or conventional financing?

For most veterans, VA loans offer significant advantages: no down payment requirement with full entitlement, no private mortgage insurance, competitive rates, and flexible credit guidelines. Conventional loans may make sense in specific situations, such as when you want to preserve VA entitlement for a future purchase or when conventional rates are unusually favorable. Our team can compare both options based on your circumstances.

Put Your VA Benefits to Work

Your military service earned you access to one of the most powerful home financing tools available. Whether you're a first-time buyer, relocating for a PCS, purchasing an investment property while occupying one unit, or building a custom home, the VA loan program offers flexibility that conventional financing can't match.

The 2026 conforming limits provide useful reference points, but they don't define what's possible with your VA benefit. With full entitlement, you can finance well beyond these figures. With partial entitlement, understanding the numbers helps you plan strategically.

VA Nationwide specializes in helping veterans navigate complex entitlement scenarios, high-value purchases, construction projects, and renovation financing. We focus exclusively on VA lending, which means our team understands the nuances that general lenders often miss.

Ready to get started? Check your eligibility, connect with our team by phone or chat, or explore your options on our homepage. We're here to help you make the most of the benefit you've earned.

*No Soft Or Hard Credit Pull Required To Check Eligibility

Sources and Official References

The conforming loan limit figures referenced on this page come from official government sources:

Federal Housing Finance Agency (FHFA), "Conforming Loan Limit Values for 2026," published November 25, 2025. Available at fhfa.gov/CLL

FHFA 2026 Conforming Loan Limit Addendum (calculation methodology)

FHFA Conforming Loan Limit FAQs

Department of Veterans Affairs, "VA Home Loan Limits" guidance at va.gov

VA entitlement information is based on current VA guidelines. Specific entitlement amounts and eligibility should be verified through your Certificate of Eligibility.

Disclaimer: This page provides general information about 2026 conforming loan limits and VA loan entitlement. Individual circumstances vary. Always verify current guidelines with a VA loan specialist, as program rules and lender overlays can change.

Official VA Resources for Veterans and Service Members

Understanding your VA loan benefit starts with accurate information from the source. The Department of Veterans Affairs maintains several resources that can help you verify your eligibility, check your entitlement status, and learn more about how the program works.

Certificate of Eligibility (COE) Your COE confirms your VA loan eligibility and shows your available entitlement. You can request one through the VA's COE portal, the eBenefits website, or by working with a VA-approved lender like our team. Most veterans can obtain their COE electronically within minutes.

VA Home Loan Program Overview The VA provides a comprehensive guide to all home loan options, including purchase loans, cash-out refinancing, and the Interest Rate Reduction Refinance Loan (IRRRL). Visit the VA Home Loans page for official program details and eligibility requirements.

Understanding Loan Limits and Entitlement For detailed information on how the Blue Water Navy Vietnam Veterans Act changed VA loan limits, and how entitlement calculations work for veterans with partial entitlement, the VA Loan Limits page offers official guidance directly from the Department of Veterans Affairs.

VA Funding Fee Information Most VA loans require a funding fee, which varies based on your service history, down payment amount, and whether you've used your VA benefit before. Some veterans are exempt from the funding fee entirely. Review current rates and exemption criteria on the VA Funding Fee page.

Contact a VA Loan Specialist If you have questions about your entitlement or need help that goes beyond what a lender can provide, the VA operates Regional Loan Centers staffed with specialists who can assist. Find your nearest center through the VA Loan Center locator or call the VA Home Loan hotline at (877) 827-3702.

These resources complement the guidance our team provides. While we handle the day-to-day details of your VA loan, the VA itself remains the authority on eligibility, entitlement restoration, and program rules.

About VA Nationwide Home Loans

VA Nationwide Home Loans (powered by The Federal Savings Bank, NMLS# 411500) focuses exclusively on serving veterans, active-duty service members, and eligible military families. Our VA loan specialists have helped thousands of borrowers across all 50 states, from straightforward purchases to complex construction and renovation projects.

We maintain expertise in VA jumbo loans, VA construction financing (one-time and two-time close), VA renovation loans, VA manufactured home loans, VA streamline refinances (IRRRLs), and VA cash-out refinancing. Our team holds individual NMLS licenses and completes ongoing education specific to VA lending guidelines.